Why choose Guaranteed Issue?

For life insurance

Our Guaranteed Issue Program streamlines the process for obtaining life insurance. With just a little paperwork, groups go through underwriting based on formulas and employee classifications, instead of lengthy medical questionnaires and exams. Guaranteed Issue can be an excellent way for employers to attract, reward and retain key employees who are in good health, with the flexibility to add more employees in the future. It is not a way to provide insurance for substandard or uninsurable employees.

For long-term care coverage

Employers can choose to apply to add long-term care to their Guaranteed Issue life insurance when they have 20 or more highly compensated key executives. Our Long-Term Care ServicesSM Rider (LTCSR) is the only true long-term care rider in a Guaranteed Issue program and provides a way for employers to offer the long-term care coverage their key executives want and need. There are additional requirements and employees will need to complete a simplified LTCSR questionnaire for coverage.

Product highlights

To qualify for Guaranteed Issue life insurance, groups will need to meet certain requirements, including:

- All members of the group must be white-collar employees, with salaries of $100,000 or more, actively working and permanent U.S. residents

- There must be no known substandard or uninsurable risks in the group

- Minimum group size of 10

- Issue ages of 20-70

- Maximum average issue age of 55

- Additional minimum participation levels must be met for voluntary plans

To qualify for Guaranteed Issue with the LTCSR, groups will need to meet all the life insurance requirements, as well as:

- At least 20 people

- Issue ages 20-65

- 100% participation of those age 65 or less

- Maximum average issue age of 50

- Long-term care monthly benefit of 1% or 2% (same for whole group)

- Long-term care acceleration percentage of 20-100% of the death benefit (same for whole group, with maximum of $1 million)

- 85% approval based on simplified underwriting (LTCSR Questionnaire)

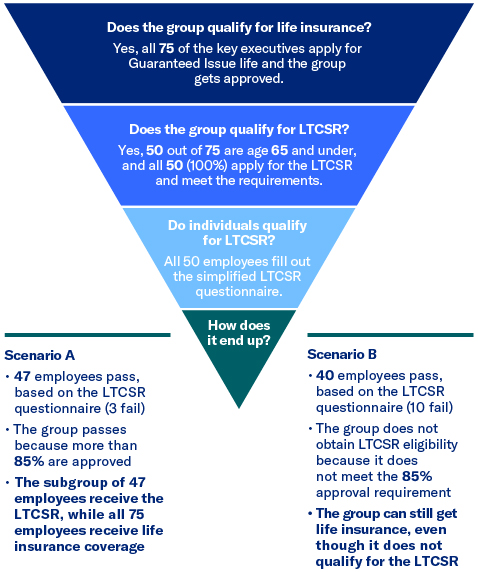

Guaranteed Issue Life with the LTCSR in action

Company ABC wants Equitable’s Guaranteed Issue life insurance and the Long-Term Care ServicesSM Rider.

- Group size: 75

Prospective client

- A variety of groups from closely held businesses to large corporations

- Cases with a large number of highly compensated key executives

- Groups where the life insurance face amount is either a flat amount for the whole group or determined by a formula such as 3 or 5 times salary

Product availability

Available with these products:

Financial Professional materials

The Long-Term Care ServicesSM Rider is available for an additional fee and does contain restrictions and limitations. A client may qualify for the insurance but not the rider, be sure to review the product specifications for details. The rider is paid out as an acceleration of the death benefit.

Life insurance products are issued by Equitable Financial Life Insurance Company (New York, NY) or Equitable Financial Life Insurance Company of America, an Arizona stock corporation with its main administration office in Charlotte, NC and are co-distributed by Equitable Network, LLC (Equitable Network Insurance Agency of California in CA; Equitable Network Insurance Agency of Utah in UT; Equitable Network of Puerto Rico, Inc. in PR), and Equitable Distributors, LLC. Variable products are co-distributed by Equitable Advisors, LLC (Member FINRA, SIPC) (Equitable Financial Advisors in MI and TN) and Equitable Distributors, LLC. When sold by New York based (i.e. domiciled) financial professionals life insurance products are issued by Equitable Financial Life Insurance Company, (NY, NY). All companies are affiliated and directly or indirectly owned by Equitable Holdings, Inc., and do not provide tax or legal advice.

References to Equitable in this page represent both Equitable Financial Life Insurance Company and Equitable Financial Life Insurance Company of America, which are affiliated companies.

Policy loans and withdrawals will reduce the face amount of coverage and the cash value of a contact. Clients may need to fund higher premiums in later years to keep the policy form lapsing.

IU-6887494.1 (08/2024) (Exp. 08/2028)