403(b) plans for educators

How a 403(b) plan can help close the retirement income gap for educators

Retirement benefits alone may not cover your future needs. Close your retirement income gap with a 403(b) plan.

If you're an educator planning for retirement, relying solely on a pension and Social Security may not be enough to meet your future financial needs.

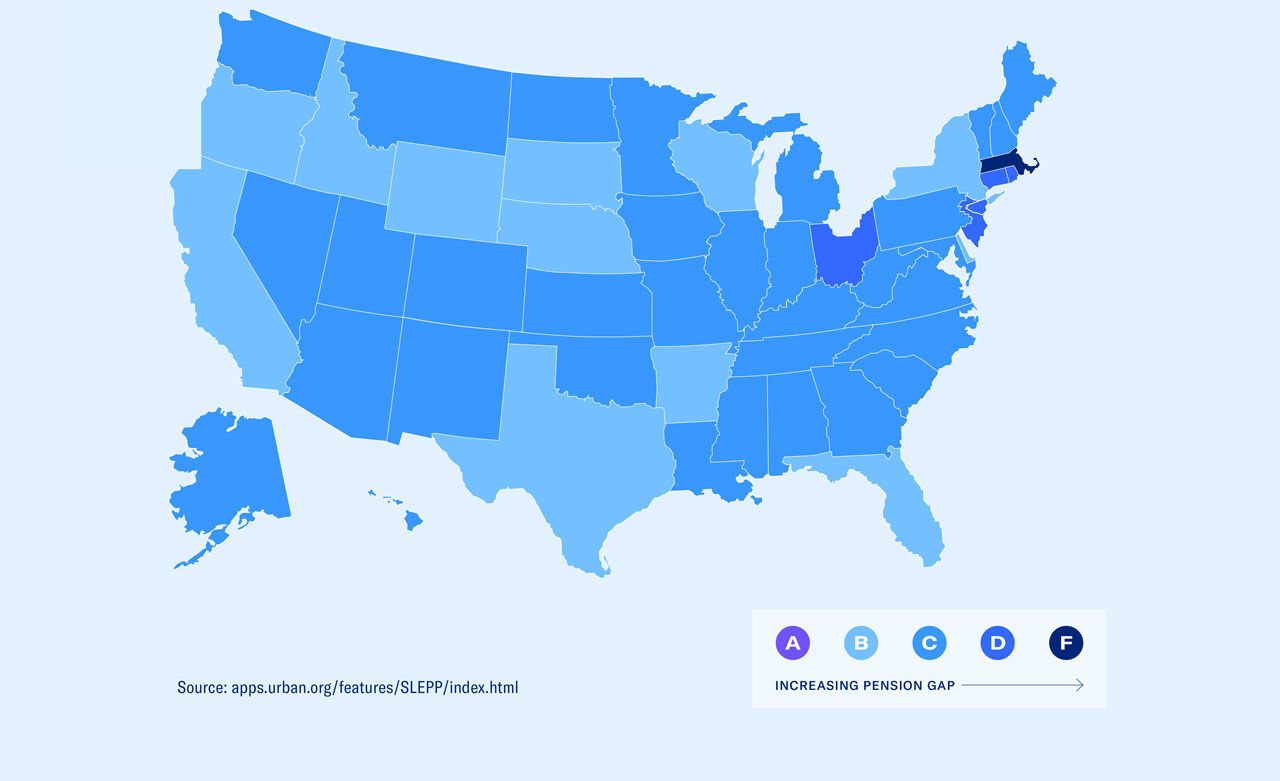

Explore your state’s pension grade

The map below shows each state’s pension grade from A to F. Darker shades indicate a larger potential pension gap for educators in that state.

Evaluate your retirement savings plan with our income calculator

Make adjustments and add in other savings to see how changes in your retirement savings plan affect your goals.

This informational calculator is not created, owned, or maintained by any Equitable Holdings, Inc. subsidiary, nor has it been determined in our own testing to be precisely accurate. Equitable Advisors and its affiliates make no representation as to the calculator's accuracy, completeness, or applicability with regard to any person's individual circumstances. The calculator provides only general estimates; its hypothetical results should not be relied upon as a basis for any financial, investment, or other decision or determination.

IMPORTANT NOTE: Equitable believes that education is a key step toward addressing financial goals, and we've designed this tool as an informational and educational resource, intended to facilitate the review of your current financial situation, based on information and assumptions provided by you. This discussion and any hypothetical results or information provided herein do not offer or constitute investment advice and make no direct or indirect recommendation of any insurance, investment, financial product or investment option. Equitable Holdings, Inc. subsidiaries do not provide tax or legal advice or services. Please consult with your tax and/or legal advisors regarding your particular circumstances. The needs, goals and circumstances of individuals are unique, and they require the individualized attention of a financial professional.

Equitable is the #1 provider of 403(b) retirement plans for educators1 for a reason.1

Frequently asked questions

Social Security is designed to replace a portion of your pre-retirement earnings, not your entire income. For most people, social security covers about 30–40% of their average lifetime earnings. State pensions are also often not enough on their own to ensure a secure retirement. Educators are strongly encouraged to contribute to supplemental retirement accounts such as 403(b) plans or IRAs to help close the gap.

For educators, the Social Security Fairness Act, enacted in January 2025, removed two key rules: one that reduced Social Security benefits for individuals who had both a pension from non-covered employment and earnings from covered employment, and another that reduced spousal or survivor benefits for those with a government pension from non-covered work. These changes allow educators to receive full Social Security benefits and ensure surviving spouses are no longer penalized, although some income differences may remain.

Employees of public schools, universities, and certain tax-exempt charitable organizations are eligible.

Employers are not required to contribute to a 403(b) plan, but some choose to offer matching or non-elective contributions.

The IRS sets annual limits on employee contributions (elective deferrals), which are adjusted annually for cost-of-living increases. Learn more

Employers are not required by law to contribute to a 403(b) plan. However, many employers choose to do so by matching or non-elective contributions.

You can use the retirement income calculator to estimate your future retirement income and see how changes in your savings strategy may affect your goals. This tool provides general estimates and should be used for informational purposes only. Learn more

Speak to your financial professional to discuss how a 403(b) plan and other strategies can help you achieve your retirement goals. If you are already a client, you can sign in or register to access account balances, transactions, and your advisor’s contact information.

Financial professionals can help you develop a personalized retirement savings plan, recommend strategies to close your retirement income gap, and guide you in making informed decisions about your financial future. Learn more

Get started

Investing in an Equitable 403(b) plan is not just a smart financial decision: it's an investment in your future peace of mind. With Equitable's proven track record and commitment to public service employees, you can trust that your retirement savings are in good hands.

Ready to start saving?

Important note: Equitable believes that education is a key step toward addressing your financial goals, and we’ve designed this material to serve simply as an informational and educational resource. Accordingly, this page does not offer or constitute investment advice and makes no direct or indirect recommendation of any particular product or the appropriateness of any particular investment-related option. Your needs, goals and circumstances are unique, and they require the individualized attention of your financial professional.

Products funding group retirement plans are issued by Equitable Financial Life Insurance Company (Equitable Financial), NY, NY or by Equitable Financial Life Insurance Company of America (Equitable America), an AZ stock company with an administrative office in Charlotte, NC. Equitable Financial, Equitable America and its affiliated companies do not offer tax or legal advice and are not endorsed by, associated, or affiliated with any school district, state agency or retirement plan.

Equitable is the brand name of the retirement and protection subsidiaries of Equitable Holdings, Inc., including Equitable Financial Life Insurance Company (NY, NY); Equitable Financial Life Insurance Company of America, an AZ stock company with an administrative office in Charlotte, NC and Equitable Distributors, LLC. The obligations of Equitable Financial and Equitable America are backed solely by their claims-paying abilities.

© 2025 Equitable Holdings, Inc. All rights reserved

GE-8605649.1 (11/2025) (Exp. 11/2029)

Why Social Security in retirement may not be the answer for educators' retirement income needs

Many educators assume Social Security will be a dependable safety net for retirement income. The truth is, Social Security was never designed to cover all your retirement income needs, and for educators, the challenges can be even greater. Limited coverage in some states, past benefit reductions, and gaps in pension plans mean relying solely on Social Security could leave you with less than expected.